Know The Products

Deposits

Liquidity Risks

Bear in mind your liquidity needs as investing in structured deposits usually tie up your funds for a period of time. An early withdrawal may result in the loss of part of your returns and/or principal.

Issuer Risks

Are you comfortable with the credit standing of the issuing bank as your funds will be deposited with them for a period of time

Market Risks

As structured deposits are linked to exposure of underlying assets/markets, their returns are therefore determined by the performance of these underlyings. Note that past performance is not indicative of future performance

Reinvestment Risks

In cases where the issuer is allowed to exercise the early redemption option, you may be exposed to the risk of having to invest your money at a lower rate compared to when you first invested and the maximum returns you receive may also be capped

Diversify risks and enhance yields

can improve overall returns of a portfolio by broadening exposure to other financial instruments without assuming excessive risk

Potentially higher returns

as compared to traditional fixed deposits, especially in a low interest rate environment

Exposure to asset/markets not easily accessible by retail investors

e.g. market indices, foreign equities, bonds, interest rates, commodities (crude oil, gold, wheat)

Protection of Principal

when held to maturity

Tenor

Structured deposits have ‘tenors’ or maturity periods that usually start from as short as a year to 10 years or longer, although such lengthy periods are rare.

When investing, you should consider the length of time you are able to set your money aside for investing

Whether the issuer has the option to redeem the deposit early

Offer Period

Structured deposits are usually offered in individual portions known as ‘tranches’.

Each tranche has either a fixed offer period or are available until the tranche is fully subscribed. However, different tranches may come with differing features and returns.

Investment Returns

What are the maximum/minimum returns from this product?

How is the return linked to the performance of the underlying assets/markets

What is the formula to determine returns; should the worst-case scenario happen, is the return acceptable?

Other features

Is there a ‘cooling off’ period for investors?

Is early withdrawal allowed and what are the costs involved?

What are Structured Deposits?

Deposit Insurance

From 1 April 2006, deposit accounts held by individuals and charities are insured by the Singapore Deposit Insurance Corporation (SDIC) for up to $20,000 in aggregate across specified accounts in each bank for each depositor under the Deposit Insurance Act. Central Provident Fund Investment Scheme accounts are separately insured for up to $20,000 in aggregate for each depositor.

Foreign currency deposits, structured deposits and accounts earmarked or held as collateral are excluded from insurance coverage.

Government Guarante

From 16 Oct 2008, all Singapore Dollar and foreign currency deposits of individual and non-bank customers in banks, finance companies and merchant banks licensed by the MAS are fully guaranteed by the Singapore government until 31 Dec 2010.

Structured deposits do not enjoy Government Guarantee.

Transactional

- Current Account with checking facility or Savings Account

- With statement or a passbook.

- Transact at branches or self-service banking facilities (egs ATM, Internet Banking, Phone Banking or Cash Deposit Machine).

- On-Demand withdrawal at branches or self-service banking facilities. Allow salary credit, GIRO, bill payment facility or NETS transaction.

Special Savings

- Internet-only account or with regular savings feature (requires a fixed sum to be deposited monthly).

- Usually pays higher interest Some restrict or disallow withdrawals.

- Those which allow withdrawals normally impose a fees or pay lower interest.

Fixed/Time Deposit

- Funds have to be maintained for a fixed tenor.

- Interest rate is also fixed upfront at placement.

- Premature withdrawal will result in no / lower interest. Some may impose a penalty fee.

Life Insurance & Investment Linked Produsts (ILPs)

Policy value fluctuates according to the performance of the underlying funds

To achieve higher potential yield, policy owner may also be exposed to higher investment risks

Investment returns are not guaranteed

Potential risk of losing capital invested

Insurance coverage charges are not guaranteed

Units may be insufficient to pay the insurance coverage charges if performance of underlying funds is very poor

Diversification

Flexibility

Professional management of investment-linked funds

Dollar Cost Averaging (applicable to Regular Premium ILP)

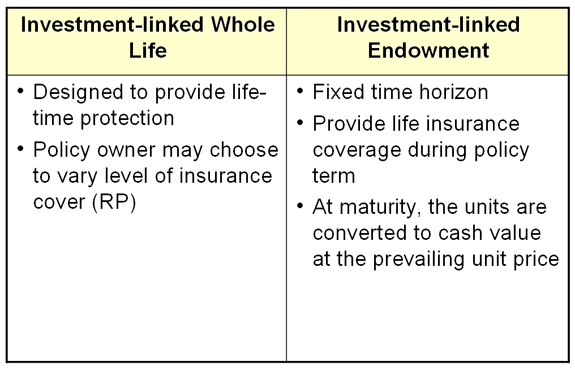

Whole Life

– A form of permanent insurance policy

– Provide coverage for the entire life of the insured

– Premiums can be paid:

–Throughout insured’s life;

–or For a limited period

Term

A form of temporary insurance

Provide coverage for a specified time period only (known as “policy term”)

Death benefit is payable when death occurs during policy term

If insured survives the policy term, nothing is paid

Endowment

A form of permanent insurance

Provide coverage for a specified time period only (known as “policy term”)

If insured dies during policy term, death benefit will be paid

If insured survives the policy term, maturity benefit will be paid upon maturity of the policy

Classification of TraditionalLife Insurance

Quick Review

Investment-linked Insurance Policy (ILP)

An life insurance policy which provides a combination of protection and investment.

Premiums are used to purchase life insurance protection and investment units in investment-linked fund(s). Policyholders can choose from the list of investment-linked funds offered by insurer.

The value of the ILP at any time varies according to the price of the underlying units, which in turn depends on how the underlying fund performs.

How does one take-up an ILP?

Types of ILP

Real Estate Investment Trust (REITs)

A listed REIT is a vehicle for investment in a portfolio of real estate assets, usually established with a view to generating income for unit holders. REITs assets are professionally managed and revenues generated from assets (primarily rental income) are normally distributed to you, as a unit holder at regular intervals. Units of listed REITs are bought and sold like other securities listed on SGX at market-driven prices.

• Portfolio Diversification REITs typically own multi-property portfolios with diversified tenant pools, which reduce the risks of reliance on a single property and tenant in the case of directly owning a real estate asset.

• Income Distribution REITs normally have regular cash flows since in most cases, most of the revenues are derived from rental payments under contractually-binding lease agreements with specific tenure.

• Participation in the Property Market Most REITs are structured around large properties. With REITs, you can own stakes in such properties.

• Professional Management REITs allow investors the opportunity to buy into properties managed by professional property management companies.

You may buy and sell listed REITs on the SGX securities market through your broker or your online trading account. Listed REITs units are traded during the normal trading hours of SGX, which is from 9am to 12.30pm, and 2pm to 5pm. There is an Opening Routine from 8.30am – 9.00am and a Closing Routine from 5pm – 5.06pm.

You need to have the following accounts:

• A securities account maintained with the Central Depository (Pte) Limited (“CDP”) or a sub-account maintained with a CDP Depository Agent;and

• A trading account maintained with a SGX Securities Trading Member Company.

REITs listed on SGX market may be purchased on margin, and on terms similar to those for other securities traded on SGX.

Returns vary for different REITs. A REIT typically distributes dividends regularly based on income generated by the properties in its portfolio. Most REITs have annual managers’ fees, property management fees, trustees’ fees and other expenses that will be deducted from their cash yields before distributions are made.

Similar to securities trading, the transaction costs include :

• prevailing brokerage commissions;

• clearing fee of 0.05% on the value of the contract (subject to a maximum of S$200); and

• Goods and Services Tax of 3% on brokerage commissions and clearing fees.

How Are Transactions In REITs Cleared And Settled?

Transactions in REITs are cleared and settled by CDP in the same manner as other securities listed on SGX, i.e. on the third business day after trade date, or T+3.

Different risk profile (investor/co)

Way for developer to:

– Raise funds

– Free up balance sheet Unlock value of ‘discounted assets’

– Capture value – bring forward profits & reduce risks

Recurring fee income

Property in

– “Bite-sized chunks”

– Liquid form (trades on SGX)

– Less concentration risk

– Ability to narrow focus to target sub-sector/region

– With professional management

Income

– Tax-exempt income for individuals

– Stability and visibility of distributions

External controls & monitoring

– Transparency / Governance

Extended Settlement contracts

A forward contract traded on the SGX Securities Market with 35 day cycle, and with 1 week overlap between monthly contracts

Allows you to long and short

Gives you leverage of 5 to 20 times with a margin of just 5% to 20% of contract value

Settlement is 3rd day after last trading day (LTD*)

Physical settlement – meaning that delivery is satisfied by taking delivery into (for long) or delivered from (for short), your trading accounts**

Trade through your securities broker online or offline

Visit www.sgx.com to get the latest prices and the cost of carry computation of each of the Extended Settlement contract.

*Investor’s cost of funding is assumed to be 7%pa ** Expenses include brokerage , clearing , access fees and GST A brokerage fee of 0.5%, clearing fee of 0.04%, access fee of 0.0075%, GST of 7% and cost of fund of 7% for initial ES margin is used in this illustration.

*Investor’s cost of funding is assumed to be 7%pa ** Expenses include brokerage , clearing , access fees and GST A brokerage fee of 0.5%, clearing fee of 0.04%, access fee of 0.0075%, GST of 7% and cost of fund of 7% for initial ES margin is used in this illustration.

Instead of selling the underlying at $17, the investor could sell at $17.40 through an ES contract for future delivery. However, this has to be weighed against the cost-of-carry (e.g. borrowing cost, interest or re-investment return foregone) from an outright sale of the underlying. For example, if bank lending rate is at 7% p.a., the interest savings foregone from the sale of 1,000 ABC shares is $17,000 x 7% x 10/365 = $32.60. Hence, the premium has to be greater than this for a profitable trade. In this instance, the implied cost-of-carry is about 0.19% of the underlying share price.

Caution: If ES contract prices moves up after the short selling, the investor could face margin calls unless he has sufficient funds to maintain the initial margin.

*Investor’s cost of funding is assumed to be 7%pa ** Expenses include brokerage , clearing , access fees and GST A brokerage fee of 0.5%, clearing fee of 0.04%, access fee of 0.0075%, GST of 7% and cost of fund of 7% for initial ES margin is used in this illustration.

Caution: ES contracts do not entitle investors with dividends or other share benefits. Investors are advised to take this factor into consideration when investing using ES contracts.

Structured Warrant

A structured warrant is a financial instrument issued by third-party financial institutions, usually banks. Structured warrants offer investors an alternative avenue to participate in the price performance of an underlying asset at a fraction of the underlying asset price, in both bullish and bearish markets

• Leverage – Warrants allow investors to gain exposure to an underlying asset at a fraction of its price. For the same investment outlay, a warrant provides an increased exposure to the underlying asset and this magnify the returns available.

• Limited downside losses – The maximum potential loss is limited o the total amount paid of the warrants, which is a fraction of the underlying asset. Potential gains, however, are unlimited for call warrants.

• Access to diverse markets – Warrants provide investors alternative avenues to participate in local and foreign-listed equities, basket of shares (e.g. ETF) or indices.

• Cash extraction – Investors can free up capital by buying the call warrants instead of the underlying assets and yet maintain an equivalent level of exposure to the underlying assets.

• Portfolio protection – Put warrants can be used to protect against a decline a portfolio’s value. This is known as hedging.

• No margin calls – Unlike other derivatives like Contract for Difference (“CFD”) or Options, warrant investors do not have to make a cash top-up if the underlying assets move adversely.

• Liquidity – All warrants listed on SGX have market makers to provide continuous bid and ask prices. Investors can buy and sell warrants anytime during market hours.

The price of a warrant is derived using option pricing models such as the Black-Scholes. There are six factors that affect a warrant price. The effects of each factor on both call and put warrants are detailed below

| Key Factors |

Change in Warrant Price |

Explanation | |

|

Call |

Put |

||

| Underlying Asset Price Increases |

↑ |

↓ |

An upside movement in the underlying asset makes a call warrant more valuable and a put warrant less valuable. |

| Exercise Price of Warrant Increases |

↓ |

↑ |

A high exercise price reduces the probability of a call warrant being exercised and increases the probability of a put warrant being exercised. |

| Implied Volatility of Underlying Asset Increases |

↑ |

↑ |

The higher the price fluctuation of the underlying asset, the greater the potential for the structured warrant to trade in-the-money. |

| Lifespan of Warrant Decreases |

↓ |

↓ |

The value of a warrant declines as the warrant’s lifespan becomes shorter. |

| Divided Yield of Underlying Asset Increases |

↓ |

↑ |

Cash payments on the underlying asset tend to decrease the value of a call warrant because it makes it more attractive to hold the underlying asset than the optionality. |

| Interest Rates Increases |

↑ |

↓ |

Interest rates affect a warrant price through the holding costs of buying the underlying assets to hedge the warrants sold. As interest rate increase, the value of the call warrant increases and the value of the put warrant decreases. |

Warrants listed on SGX are primarily European-style and may only be exercised on the expiry date. At expiry, the settlement of the warrants is usually made in cash rather than a purchase or sale of the underlying asset.

| Types | Call Warrants | Put Warrants |

| Market View | A Bullish View of the underlying asset | A Bearish View of the underlying asset |

| Rights of Warrant Holders | Holders have the right, but not the obligation, to buy the underlying assets from the issuer at a predetermined exercise or strike price on the expiry date | Holders have the right, but not the obligation, to sell the underlying assets to the issuer at a predetermined exercise or strike price on the expiry date |

| Lifespan | Warrants have an average lifespan of 3 to 9 months. Warrants are also offered with longer tenure between 1 to 3 years. | |

| Settlement if warrants expire in-the-money | Cash settled if the settlement price is above the exercise price | Cash settled if the settlement price is below the exercise price |

| Potential Loss | Total investment outlay | |

• Limited lifespan – Unlike the underlying asset, warrants have a limited lifespan and will expire. If they expire at-the-money or out-of-the-money, investors holding onto these warrants will lose their entire investment capital used to purchase the warrants.

• Leverage – Being geared instruments, returns can be magnified if the underlying asset moves in the direction favourable to the warrant-holder’s view. However, losses can also be high if the underlying moves against the warrant-holder’s view.

• Issuer risk – Warrant holders are unsecured creditors of issuers. They have no preferential claim to any assets that an issuer may hold in the event the issuers are unable to fulfill their obligation.

• Currency risk – If the price of the underlying asset is denominated in a foreign currency, investors will be exposed to foreign exchange rate fluctuations.

• Market risk – The market value of a warrant is susceptible to other prevailing market forces including the demand and supply of the warrants.

• Suspension from Trading – Trading of warrants will be halted or suspended if the underlying stock is halted or suspended. Warrants investors will not be able to unwind their positions in such circumstances.

Please visit www.sgx.com/warrants for more information on SGX-listed structured warrants or download the Investor Guide to Structured Warrants.

This document is not intended for distribution to, or for use by or to be acted on by any person or entity located in any jurisdiction where such distribution, use or action would be contrary to applicable laws or regulations or would subject SGX to any registration or licensing requirement. This document is not an offer or solicitation to buy or sell, nor financial advice or recommendation for any investment product. This document is for general circulation only. It does not address the specific investment objectives, financial situation or particular needs of any person. Advice should be sought from a financial adviser regarding the suitability of any investment product before investing or adopting any investment strategies. Further information on this investment product may be obtained from www.sgx.com. Investment products are subject to significant investment risks, including the possible loss of the principal amount invested. Past performance of investment products is not indicative of their future performance. Examples provided are for illustrative purposes only. While SGX and its affiliates have taken reasonable care to ensure the accuracy and completeness of the information provided, they will not be liable for any loss or damage of any kind (whether direct, indirect or onsequential losses or other economic loss of any kind) suffered due to any omission, error, inaccuracy, incompleteness, or otherwise, any reliance on such information. Neither SGX nor any of its affiliates shall be liable for the content of information provided by third parties. SGX and its affiliates may deal in investment products in the usual course of their business, and may be on the opposite side of any trades. SGX is an exempt financial adviser under the Financial Advisers Act (Cap. 110) of Singapore. The information in this document is subject to change without notice.

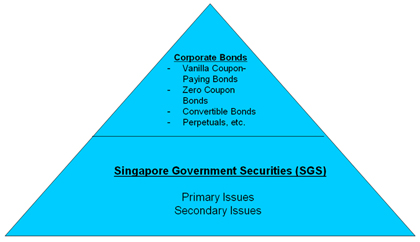

Bonds

Issuer Risk

Subject to issuer risk, a bond will return the bond investor his/her principal back at maturity.

What this means is if the issuer goes bankrupt, a bond investor will likely not get back his principal.

Price Risk

Bond Prices are affected by interest rate movements. Typically when interest rates rise, bond price falls.

Investors should be aware that the price of their bond may fall due to interest rate rises.

Reinvestment Risk

Although investors do receive coupons on a regular basis, they may not be able to reinvest the coupons at the same rate that they received the coupons at.

- Present value of the coupons and principal in the holding period.

- Bond prices are typically quoted as a percentage eg. 100.3% or 98.2% of par value of bond.

- Bonds with prices quoted above 100% are trading at a premium.

- Bonds with prices quoted below 100% are trading at a discount.

- Bond prices move in the opposite direction of interest rates i.e. if interest rates rise, the price of a bond will fall and vice-versa.

- A bond typically pays regular coupon (interest) to customers based on a fixed schedule.

- Subject to issuer risk, a bond will return the principal back to the customer at maturity.

- A bond has varied tenor (from anything as short as a few weeks to as long as 30 years), so an investor should be able to find a bond that suits his investment horizon.

- Bonds are debt instruments issued by a company or a government entity (‘Issuer’).

- The Issuer will pay a coupon (interest) to the bond investor based on a schedule. This schedule can be on a quarterly, semi-annual or annual basis.

- At maturity, the Issuer will return the principal back to the investor.

Unit Trust (UTs)

Know Your Investment Needs

Determine Your Risk Profile

Determine The Time You Would Like to Stay Invested

How UTs Fit In Your Investment Portfolio

Know the Risks of UTs

Fund Evaluation & Performance

UT Fee Structure

Other Considerations

Low savings deposit rates environment

Inflation eats into purchasing power

Potentially provides additional source of income

Aim to meet medium and long term financial needs

The need to plan for your retirement

The CPFIS gives members the opportunity to invest their CPF savings to enhance their retirement funds:

- Investments in UTs can be made through the Ordinary (OA) and Special Accts (SA)

- From 1st May ‘09, one has to set aside the first $30,000 in SA before the remaining can be used for investments. Since 1st Apr ’08, $20,000 to be set aside in OA

As of 13 Jan ‘09, there were approx. 129 funds available for investments under the CPFIS.

Local Banks

Foreign Banks

Private Banks

Securities Firms

Insurance Companies

Independent Financial Advisers

Internet Intermediaries

Direct distribution

Types of UTs

Note: These funds may be further classified into Different Currencies, for Retail/Accredited Clients and Open/Closed-ended Structures

UTs/Mutual Funds are professionally managed investment funds which pool the financial resources of individual/corporate investors with similar investment objectives.

Aggregate sums are used by the funds to make large scale investments in a selected investment portfolio which comprises stocks, bonds and/or other assets with the investment objective of the fund in mind.

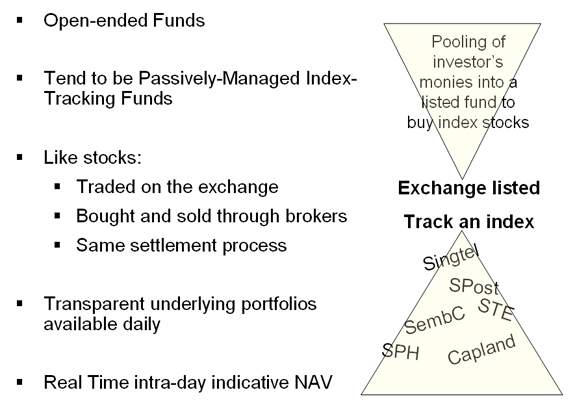

Exchanged Traded Funds (ETFs)

Exchange Traded Funds (ETFs) are often described as instruments that give investors the benefits of diversification at a low cost. While this may be attractive, it is important to know that ETFs, being investment products, are not free from risk elements.

It is also important to know that not all ETFs have the same structure and level of complexity. Some ETFs come with more complex structures, and may not invest directly in the assets or components of the indices that the ETFs track. Depending on the structure of the ETF, some ETFs are not able to replicate the returns of the underlying asset or index as closely as others, and some ETFs may be exposed to more risks than others.

This Guide aims to help you understand what ETFs are and what you should consider before investing in them. It highlights the benefits and risks of investing in ETFs, what you should look out for in the prospectus and other important information.

ETFs are open-ended investment funds listed and traded on a stock exchange. Similar to trading any stock, you can buy and sell ETFs through any stock broker at market price throughout the trading day.

The objective of an ETF is to track a specific benchmark such as a stock or commodity index or commodity price. As such, ETFs are passively managed by professional fund managers and their expense ratios are lower than those of actively managed unit trusts since they track and do not try to outperform the underlying benchmark.

Below are examples of assets or indices tracked by ETFs available on the Singapore Exchange (SGX):

• Commodity and commodity index – These ETFs are intended to provide exposure to only one type of commodity or a basket of closely related commodities. As such, they may not be as diversified as ETFs linked to a broad-based equity index.

• Bond index – ETFs can also track a specific bond index. These ETFs provide exposure to the fixed income market.

• Equities

– Long stock index – Some ETFs track the movements of a stock index, such as the Straits Times Index (STI). This means that if the index increases in value by 2%, the ETF is intended to increase by 2%, less any fees.

– Inverse (or ‘short’) index – These ETFs track the movements of a short index. The short index moves inversely to its corresponding long index on a daily basis. So if the long stock index drops by 2%, the short index will increase by 2% less any fees. However, this relationship holds only on a day-to-day basis. The movement of a short ETF may not be equal to the simple inverse of the long index when measured over a period of more than one day. These ETFs are generally not intended for long term investments and are generally not suitable for retail investors who plan to hold them for longer than one day, particularly not in volatile markets.

ETFs are continually being listed on SGX, covering worldwide equity markets such as Singapore, India, North Asia, ASEAN, United States, Eastern Europe, Latin America and emerging markets, as well as commodities including gold.

Get the latest list of ETFs listed on SGX on ww.sgx.com

TIP: Do not assume that all ETFs come with low risks and are intended for long term investing. Read your prospectus and research reports to understand three key areas:-

– The investment objectives (in particular whether the specific ETF you intend to invest in is meant to track indices on a daily basis only and thus only suitable for short term investing);

– The underlying exposure; and

– Its expected returns and volatility.

ETFs can be structured differently to track the same underlying index. For example, some ETFs replicate the index by investing in the index’s component stocks. Others may invest in a representative sample of stocks from the index they are designed to track.

Some ETFs may use other more sophisticated instruments like swaps and participatory notes in addition to holding a basket of representative stocks or collateral. This may be because they wish to track the underlying index more efficiently or because it is not possible for the ETF to invest directly in the index’s component stocks.

However, this exposes the ETF to counterparty risk from the swap counterparty or participatory note issuer. This means that in the event of bankruptcy or insolvency of the counterparty, the ETF may incur losses and the extent of loss will depend on fund’s exposure to the swap counterparty. For example, UCITS III compliant ETFs(1) are allowed to use derivatives (including swaps), although they must limit their exposure to a single counterparty to 10% of its net asset value (NAV), most commonly via the posting of collateral. In other words, the fund is limited to the losses that are related to the default of the swap counterparty, to a maximum of 10%, should the collateral maintain its value after a default. There are also other ETF structures which require posting of collateral by the swap counterparty to mitigate the extent of loss, should the counterparty default.

(1) UCITS III is the regulatory regime for funds in Europe. UCITS refers to undertakings for collective investment in transferable securities.

TIP: Always find out how the ETF you are considering works. Remember that not all ETFs have the same structure and level of complexity.

- Read the “Investment Approach” and “Risks” portions of your prospectus for information on the various risks of the specific ETF you intend to invest in. Note that the risk elements may differ greatly between ETFs depending on their structure.

- Consider if the ETFs structure and risk profile suit your risk appetite and investment time horizon.

- Do not invest in an ETF if you do not understand or are not comfortable with the structure.

dvantages of ETF!

Benefits of ETFs

Diversification: Compared to stocks, ETFs on stock indices allow investors to avoid stock-picking by providing exposure to a diversified portfolio of stocks through a single transaction at an affordable price. However, not all ETFs are broadly diversified. The extent of diversification benefits depends on the constituents that make up the fund portfolio. For example, ETFs that are meant to track the performance of a single commodity or a basket of closely related commodities will not be as diversified as those broad-based equity index ETFs.

In the case of long only country indices ETFs, they retain relevant exposure to the country or market. For example, a country’s key index like the Straits Times Index (STI) for Singapore aims to reflect the economic composition and market structure of the economy. Over time, index providers adjust the indices to maintain this relevance according to the rules set in the index methodology. As such, investors holding these ETF units will be appropriately diversified.

Adding ETFs in your investment portfolio can help diversify unsystematic risk. This refers to the risk of price change due to the unique circumstances of a specific stock as opposed to circumstances in the overall market. However, as with all other investment products, ETFs cannot eliminate market risk. Refer to the section on Risks of ETFs for more information

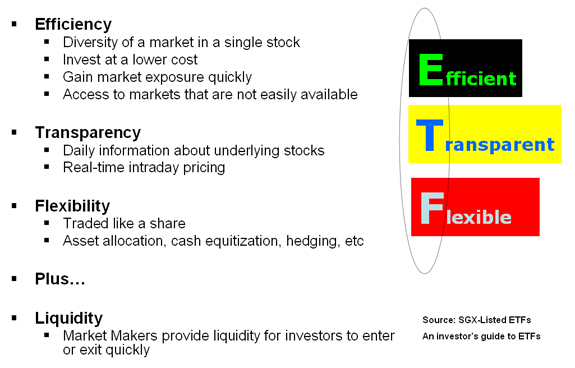

Cost Efficiency: Compared to unit trusts, investing in ETFs is more cost-efficient as investors do not need to incur the typical sales charge of 3% to 5%. The brokerage commission paid is similar to that paid when buying or selling stocks. The expense ratios for ETFs also tend to be lower than unit trusts, usually due to the annual management fee being typically less than 1%. Management fees for unit trusts generally range between 1% and 2%.

Transparency and Flexibility: The process of buying or selling an ETF is transparent and flexible, just like trading stocks listed on the exchange. Investors can access information on the ETF prices and trade ETFs throughout the trading day. Moreover, investors can employ the traditional techniques of stock trading including stop-loss orders, limit orders, margin purchases, etc. This transparency and flexibility cannot be achieved with unit trusts as investors can only transact at one price calculated at the end of each day.

See Table 1 for a comparison of features between ETFs, stocks and unit trusts.

Table 1: Comparison of features between ETFs, Stocks & Unit Trusts

|

ETFs |

Stocks |

Unit Trusts |

|

| Diversification |

Yes |

No |

Yes |

| Sales Charges |

None |

None |

3 – 5% |

| Management Fees |

Less Than 1%* |

None |

1 – 2% * |

| Intra-day Price Transparency |

Yes |

Yes |

No |

| Traded Through Broker |

Yes |

Yes |

No |

| Brokerage Commission |

Yes |

Yes |

None |

| Settlement |

Third Business Day after Trade Date |

Third Business Date After Trade Date |

Upfront |

*ETFs and other unit trusts may have to incur other expenses, such as legal or trustee fees, which may be payable from the fund separately from the management fees.

Some of the risks associated with investing in ETFs include:

Investing for longer than the Intended Tracking Period: Inverse or short ETFs are intended to track the movements of a short index. The short index moves inversely to its corresponding long index on a daily basis. This means that the performance of the short index may differ greatly from the inverse performance of the long index when measured over a period of more than one day. These ETFs are generally not intended for long term investments and are generally not suitable for retail investors who plan to hold them for longer than one day, particularly not in volatile markets. Investors should familiarise themselves with the investment objective in the prospectus to see if the specific ETF they intend to invest in is meant to track indices only on a daily basis.

Market Risk: Investors are exposed to market risk or volatility of the specific benchmark which the ETF tracks. For example, the performance of an ETF tracking the STI will be directly affected by the price fluctuations of the constituent stocks of the STI.

Counterparty Risk: Where an ETF uses a swap or participatory note structure, investors are exposed to counterparty risk. This means that in the event of a bankruptcy or insolvency of the counterparty, the ETF could incur significant losses. For some ETFs registered as UCITS III, this loss could be limited to 10% of their total NAV, but for others, this loss could be much larger.

Tracking Error: The fund manager of the ETF may not be able to exactly replicate the performance of the specific benchmark due to various fees, investment constraints, timing differences and other factors. This is known as tracking error. As a result, the change in the NAV of the ETF may not exactly follow the price changes of the benchmark.

Market Price not reflecting NAV: The NAV of the ETF may itself be different from the market price, which is affected by demand and supply. The designated market maker works with the fund manager to create new units or redeem units to meet market demand and bring the market price in line with the NAV of the ETF. However, this may not erase the difference between the market price and the NAV entirely.

Foreign Exchange Risk: For ETFs denominated in foreign currencies, investors should be aware that foreign exchange rate fluctuations may affect the returns if they wish to receive their returns in Singapore Dollars. In addition, some of the assets of the ETFs may not be denominated in the same currency the ETF is traded in.

Liquidity Risk: As with all investments, investors should be aware of liquidity risk – the risk arising from difficulty in buying or selling units in an ETF. Liquidity in ETFs is usually provided by a market maker who will provide continuous bid-ask prices throughout the trading day. However, in the event that the market maker fails to perform its duty due to insolvency or other considerations, liquidity in the ETF is not guaranteed. The ETF may then have a large spread between bid-ask prices. However, unit trusts generally have better liquidity as the fund manager is legally bound to redeem units on each dealing day, except in extreme circumstances described in the prospectus.

Conclusion

As with any other investment product, investors should also take time to understand the product and consider whether it is suitable for them. Here are a few key things you should check before deciding whether to invest in an ETF.

1) What does the ETF track?

Do not assume that all ETFs come with low risks and are intended for long term investing. Read your prospectus and research reports to understand three key areas:

- the investment objectives (in particular whether the specific ETF you intend to invest in is meant to track indices on a daily basis only and thus suitable for short term investing);

- the underlying exposure; and

- its expected returns and volatility.

2) How is the ETF structured and what does it invest in?

Remember that not all ETFs have the same structure and level of complexity. Read the “Investment Approach” and “Risks” portions of your prospectus for information on the various risks of the specific ETF you intend to invest in. Note that the risk elements may differ greatly between ETFs depending on their structure.

Do also find out:

- Who is the Fund Manager and the Market Maker? (For e.g. manager’s track record in managing ETFs, the quality of market making by the market maker in terms of providing competitive bid/ask spread. If either fails to perform their duty due to insolvency or other considerations, liquidity in the ETF is not guaranteed.)

- What are the trading specifications (i.e. board lot size & currency denomination)?

- What are the expected costs (i.e. brokerage commission, management fees & expense ratio)?

3) What level of tracking error is likely to occur and how would this error impact your returns?

Ask your financial adviser or broker:

- how you can monitor the tracking error regularly;

- what measures are in place to manage such errors; and

- what risks and costs come with these measures.

4) Does the ETF’s structure and risk profile suit your risk appetite and investment time horizon?

5) How does the ETF you are considering compare with other investment options?

Last but not least, if you find that you do not understand the ETF or are not comfortable with its structure and risks, do not invest in it.

This information is provided by the Singapore Management University Sim Kee Boon Institute for Financial Economics and the Monetary Authority of Singapore (MAS) as part of the MoneySENSE national financial education programme.

Foreign Exchange (FX)

Unlike other financial markets that operate at a centralized location (i.e., the stock exchange), the worldwide Forex market does not have a central location. It is a global electronic network of banks, financial institutions and individual Forex traders.

FX market is 24 hrs market, Major world trading starts each morning in Sydney and Tokyo, then moves west to Hong Kong and Singapore, continuing to Europe and finishing on the West Coast of the U.S.

– Max. intensity at 8:00 and 14:00 (GMT)

– Min. intensity at 4 (Tokyo lunchtime) and 23 (end of NY)

FX market is the largest and most liquid market in the world, with a daily turnover of 4.5 trillion USD last year.

For comparison, the GDP of US 2008 is 14.4 trillion USD.

Golden Rules for investment in FX market:

– The exchange rate is determined through the interaction of market forces dealing with supply and demand.

– The value of a currency, in the simplest explanation, is a reflection of the condition of that country’s economy with respect to other major economies.

More specifically, two primary factors that affect supply and demand are

– Interest Rates, usually set by central bank. Increasing or decreasing interest rate is always the top focus of currency traders. The higher the interest rate, the more valuable the currency would be.

– The Fundamental indicators of the originating country’s economy as a whole. such as foreign investment, PPI, CPI, GDP, and the trade balance, echo the overall health of the economy, and alter the supply and demand for that currency. The stronger the economy, the more valuable the currency would be.

– High sensitivity to government policies, especially central bank decisions. The central bank usually step in to help restore order in the market in the event of excessive currency rate volatility.

– High sensitivity to macroeconomic indicators, focusing on big pictures of certain country, ignoring details about specific stocks and industry. The skills to interpret macroeconomic news are sophisticated.

– High volatility than equity market (because of margin trading), 24 hours running make it hard to monitor real time price quote.

– Retail investors are high recommended not to take excessive risk in FX market.

– Minimum capital requirement.

– It is always quoted in pairs like the USD/SGD. (the US Dollar and Singapore Dollar)

– Interest is payable or receivable due to the differences between the interest rate of 2 currencies.

– It is generally quoted in multiple sizes of 100,000 of the first currency.

– Commission is charged for each transaction or through the spread of the currency pair.

– Interest rate differential also called swaps points are credited or debited daily.

– It begins each day in Sydney, and then moves around the globe as the business day begins in each financial center, first to Tokyo, then London and New York.

– Unlike any other financial market, investors can respond to currency fluctuations caused by economic, social and political events at the time they occur – day or night.

– Familiarity

– Liquidity and spreads

– Volatility

– Cost of carrying the trade

– Availability of information