Date: April 28, 2023

It is well known that Singaporeans love to invest in property. Everyone aspires to own their own home, and many buy a HDB flat with ambitions to later upgrade to a private property. Many also buy a second home for rental income and capital appreciation and to be sure, property as an asset class has historically performed very well which adds to the appeal of the sector.

However, the amount of money needed to buy a property is substantial and there are many legalities that need to be observed, such as payment of stamp duties, legal fees and valuation charges.

Moreover there are many other property assets that can offer decent returns like warehouses and office buildings because of the rental income they earn from tenants. How might an interested investor gain exposure to these sectors?

What are REITs?

Real estate investment trusts (REITs) are investment vehicles which own and operate income-generating real estate such as retail malls, office buildings, healthcare facilities, hotels and warehouses. Investors in REITs gain exposure to these properties for a relatively small capital outlay.

Most of a REIT’s returns come from its distribution per unit (similar to dividend per share) although capital gains are also possible if the REIT’s price rises.

REITs generate revenue through the rental income paid by tenants who occupy the REIT’s properties. From time to time, REITs may also generate a profit by buying property at a relatively low price and selling it later at a relatively higher price. This is called asset recycling.

You can invest in REITs the same way as you would invest in stocks, through your broker. There are many REITs traded on the Singapore Exchange (SGX).

It is important to note that REITs are governed by the Securities and Futures Act and are regulated by the Monetary Authority of Singapore in accordance with the Code on Collective Investment Schemes.

They should be differentiated from Business Trusts which may also own income-generating assets but are governed by the Business Trusts Act.

Why invest in REITs?

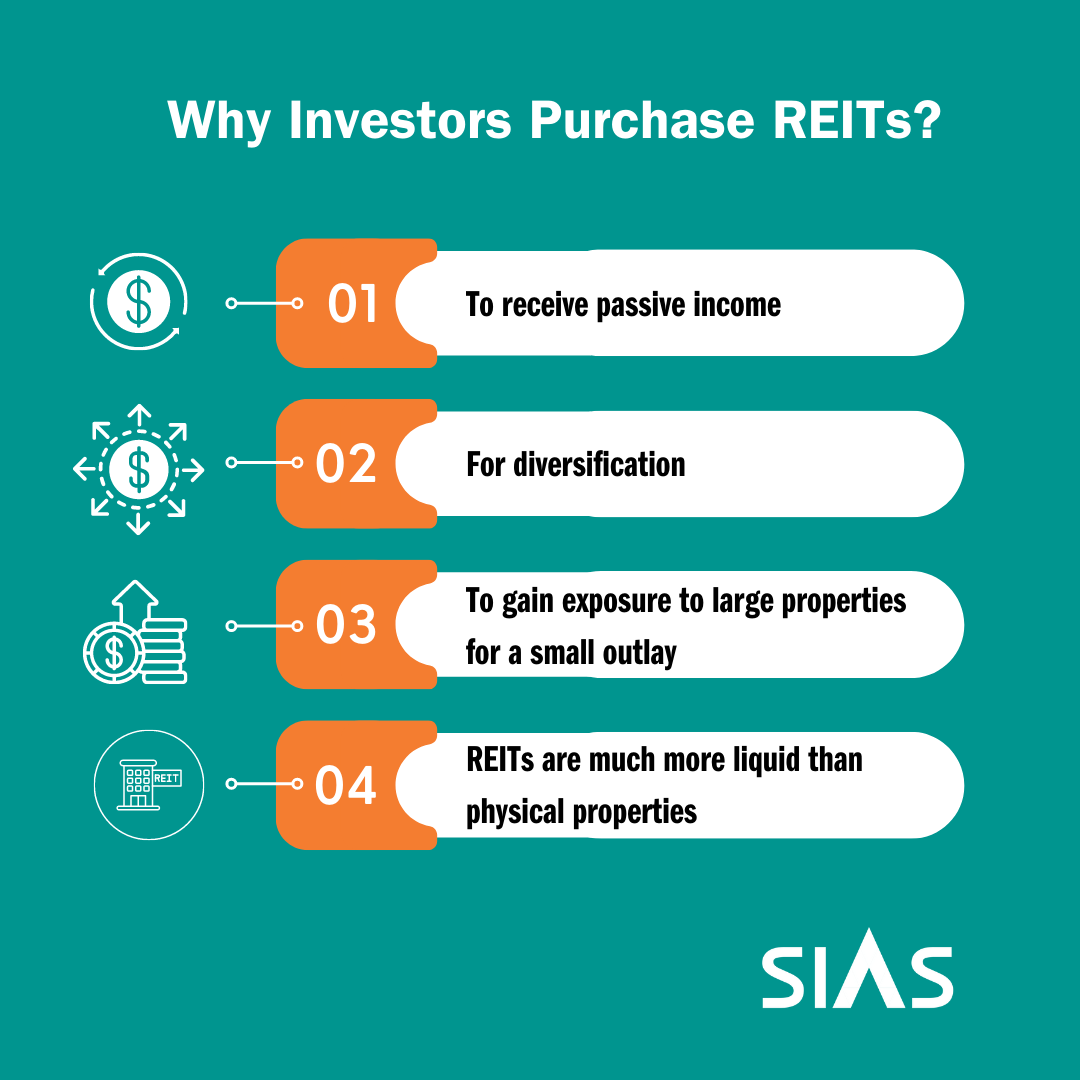

Investors buy REITs for the following reasons:

- To receive passive income: Singapore REITs do not need to pay tax if they pay out at least 90% of their profit to unitholders. This incentive is referred to as enjoying tax transparency treatment from the Inland Revenue Authority of Singapore, and means that REITs can, most of the time, be relied upon as a source of passive and regular income.

- For diversification: Investing in a REIT means you are invested in the diversified pool of assets that the REIT owns. In this way the investor avoids being exposed to only one property.

- To gain exposure to large properties for a small outlay: it would be very expensive for an individual investor to afford direct investment in say, a healthcare facility or hotel. However, buying units in a REIT allows investment in such properties in much more affordable chunks.

- Because they are much more liquid than physical properties: It is much easier to buy and sell a REIT than physical properties. As noted earlier, REITs are traded on SGX so they can be bought or sold throughout the trading day.

What are the risks?

The market price and distribution of a REIT reflects the market’s overall confidence in the economy, the state of the property market, the returns of the property owned by the REIT, the interest rate environment and the ability and competence of the REIT’s management.

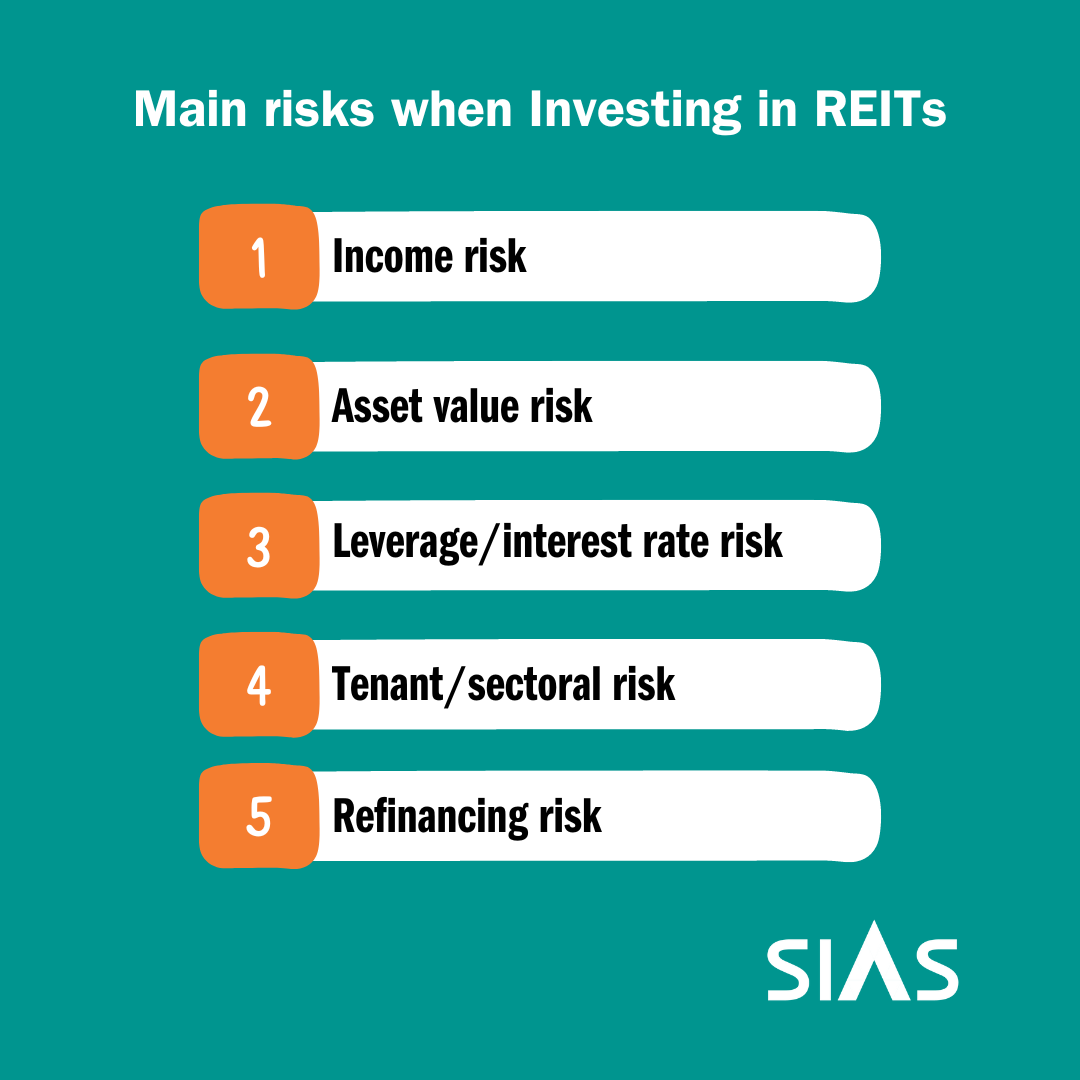

These are the main risks when investing in a REIT:

- Income risk: because of a drop in rental revenue and/or falling occupancy. Distributions are not guaranteed and are subject to fluctuations in the REIT’s income. For example, a REIT’s rental income may be affected if tenancy agreements are renewed at a lower rental rate than previously, or the occupancy rate has fallen.

- Asset value risk: this occurs when asset values fall because of downturn in the property market.

- Leverage/interest rate risk: REITs tend to have large borrowings in order to buy their assets. If interest rates rise suddenly, the interest expense to REITs will also increase, thus impacting their profits. Also. rising interest rates could make other instruments more attractive and lead to selling pressure on REITs.Under current MAS rules, borrowing by REITs cannot exceed 50% of their total assets.Over the course of 2022, note that REITs suffered because interest rates were raised quickly all over the world by central banks who were looking to curb rising inflation.

- Tenant/sectoral risk: As REITs depend on the rental income from their tenants, any cash flow issues experienced by their tenants may negatively impact their revenue. For example, many REITs, especially those owning retail malls, performed badly during Covid-19 as many tenants had to suspend operations.Depending on the type of property they own, different REITs may face different sectoral risk factors. For example, a REIT which invests mainly in hotels (i.e. a hospitality REIT) is dependent on the number of visitors patronizing its hotels and this fell sharply during Covid-19.Also, the current trend towards working from home is affecting demand for office space and this will adversely impact office REITs.

- Refinancing risk: As REITs distribute a large amount of their income to unit holders, they may not have the ability to build up cash reserves to repay loans as they fall due. To refinance, they may need to borrow more (through bank borrowings or bond issuances) or undertake equity fund raising activities such as rights issues or private placements.

Some considerations when assessing the health of REITs

In general, REITs which have anchor tenants (e.g. a supermarket or cinema) or globally recognized brands as tenants are likely to have signed long-term, multi-year rental agreements and should not be too badly exposed if a tenant suffers cash flow problems.

By the same token, REITs which have a large diverse pool of small tenants (i.e. retail shopping centres) may face a more challenging environment.

A REIT’s ability to meet its financial obligations can be measured using leverage ratios. One common leverage ratio is the debt-equity ratio. By comparing a REIT’s total liabilities to its shareholder equity, we can get an idea if a REIT’s debt level is too high.

Another useful measure to look at is the REIT’s interest coverage ratio. This measures the REIT’s ability to meet its interest payments and is calculated by dividing its earnings before interest and taxes (EBIT) by its interest expenses. If the ratio is above 1, then even if the REIT is unable to repay the principal amount of its debt, it is still, theoretically, able to cover its interest expenses.

What retail investors should consider before investing in REITs

Investors should do their homework by reading the REIT’s issue prospectus and as many research reports as possible. They should check the quality of the properties in the REIT and also consider the quality of the people and parties behind the REIT.

Not all REITs are the same. Besides the different sectors, the strength of the sponsor also makes a difference in the quality of a REIT. Sponsors are usually large, well-established property companies which can help support the REIT by providing a regular pipeline of properties as well as help secure favourable financing terms.

Another key player is the REIT’s manager, who is sometimes described as the brains behind the REIT. Investors should check who the manager is and its track record.

Always remember to diversify and not put all your eggs in one basket.

Subscribe to Newsletter

Subscribe to SIAS Mailing List and get updates to all upcoming events and news

By clicking submit, you agree to our privacy statement, collection, use and/or disclosure of your personal data to the extent necessary to provide you with this service.