Date: February 21, 2022

To: Mapletree North Asia Commercial Trust Management Ltd., manager of

Mapletree North Asia Commercial Trust

Through: Ms. Cindy Chow, Executive Director and Chief Executive Officer

Questions to Mapletree North Asia Commercial Trust (“MNACT”)

On December 31, 2021, Mapletree Commercial Trust (“MCT”) and MNACT announced a merger to create a flagship commercial REIT, to be named Mapletree Pan Asia Commercial Trust (“MPACT”). MCT will acquire all the issued and paid-up units of MNACT by way of a trust scheme of arrangement. On paper, the scheme consideration is $1.1949 per MNACT unit with the scheme issue price of new MCT units at $2.0039. MNACT unitholders will have the option to receive 16% in cash ($0.1912), along with 0.5009 new units per MNACT unit.

In order to help MNACT unitholders better understand the proposed merger, SIAS has prepared the following questions for MNACT:

Why do a merger? And why now?

MNACT has been successful in diversifying into new key gateway markets since 2018. In the joint announcement, the justifications for the merger include allowing MNACT access to the “stable and resilient Singapore market” and achieving higher financial capability and flexibility to accelerate growth (due to an enlarged base).

- It is not apparent that there are any operational synergies in the proposed Merger with MCT. Can the MNACT Manager share more on why this Merger is necessary other than having access to Singapore market? Has the MNACT Manager carefully considered whether this Merger is in line with MNACT Unitholders’ expectations and/or needs?

Unitholders should also note that the pro forma NAV of MNACT will decrease from $1.265 to $1.10 as at 30 September 2021 (1H FY21/22), a drop of 13%. Pro forma DPU will also decrease from 3.426 cents per unit to 2.85 cents per unit (cash and scrip) for the six months ended 30 September 2021 although the pro forma aggregate leverage will improve from 41.4% (as reported) to 39.2% (cash and scrip).

- Would MNACT and its unitholders be better served if the MNACT Manager forges ahead with its strategy of repositioning of MNACT and only consider a merger at an offer price above its NAV?

Deal Process

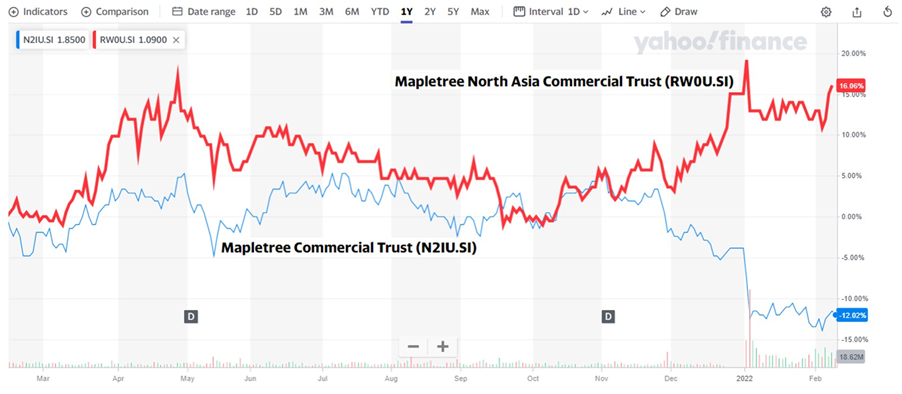

Both REITs called for a trading halt on December 28, 2021 before the joint announcement on December 31, 2021. Mapletree Investments Pte Ltd is the common sponsor of both MNACT and MCT. In fact, if one were to look at the relative performance of the two REITs in the past year, MNACT has performed as strongly as, if not stronger than, MCT. (See Appendix A)

- Can the MNACT Manager elaborate further on the decision making and negotiation process with MCT and how independent was the process before the Merger was proposed to independent MNACT Unitholders for a vote? Were good corporate governance protocols adhered to? What was Mapletree Investments Pte Ltd (“MIPL”, or the “Sponsor”)’s role during the negotiations and what were the safeguards put in place given that the two REITs have a common Sponsor?

- Is the MNACT Manager actively seeking competing bids or has it signalled to the market that it is prepared to consider superior offers? For the avoidance of doubt, can the MNACT Manager confirm that it has not entered into any non-solicitation and/or no-shop provisions? Did the MNACT Manager consider other alternatives, such as sale of key assets coupled with a faster pace of capital recycling, to crystallise value for MNACT Unitholders?

MNACT’s portfolio and performance

Festival Walk and Gateway Plaza, account for more than 70% of MNACT’s portfolio, continued to report lower average rental rate. Rental reversion for Festival Walk accelerated from negative 21% to negative 30%. For Gateway Plaza in Beijing, the rental reversion was from negative 7% to negative 24%. A major tenant at Gateway Plaza is due for renewal in December 2023.

- Is the proposed Merger a way to leverage the resilient MCT’s portfolio at a time when Festival Walk and Gateway Plaza are underperforming? What are the plans and asset enhancement potential for these two assets? Regardless of the outcome of the proposed Merger, are these two assets considered core to the REIT?

Management fee structure

A new management fee comprising of a base fee of 10% of distributable income (originally 0.25% of total assets) and a performance fee of 25% of the y-o-y growth in DPU (originally 4% of net property income) is being proposed. In September 2020, the manager of MNACT waived its entitlement to any performance fees until such time that the DPU of MNACT (on a standalone basis) exceeds the threshold DPU of 7.124 cents.

- Will the performance fee waiver be “carried forward” to MPACT and that no performance fee will be charged on the distributable income from the MNACT assets until the threshold DPU (or an equivalent measure based on distributable income from the MNACT assets) is met?

David Gerald

President and CEO

SIAS

Click here to see reply from MNACT

Appendix A: Relative performance of MNACT and MCT in the past twelve months

(Source: Yahoo Finance)

Note: Both REITs called for a trading halt on December 28, 2021 before the joint announcement three days later on December 31, 2021. Mapletree Investments Pte Ltd is the common sponsor of both MNACT and MCT.

Subscribe to Newsletter

Subscribe to SIAS Mailing List and get updates to all upcoming events and news

By clicking submit, you agree to our privacy statement, collection, use and/or disclosure of your personal data to the extent necessary to provide you with this service.