Date: November 22, 2021

As Warren Buffett, puts it, “Risk comes from not knowing what you are doing.” Indeed. How many of us can claim that we have not been tempted to jump the gun when we read about new-kid-on-the block investment opportunities. Our subject of interest, Special Purpose Acquisition Companies (SPACs), is the latest and possibly trendiest member to join the financial scene in Singapore. Like any new addition to the circus, every investor is undoubtedly curious about them. But just like those lengthy terms and conditions in contracts that nobody fancies scrutinising, we all want a crisp overview of the basics. Here is my attempt to do so.

What is a SPAC?

It is a shell company formed to raise capital through an initial public offering (IPO) to eventually acquire another company. Unlike a typical publicly listed company, a SPAC has no business operations. Its assets are typically limited to the funds from the IPO. A SPAC functions as a vehicle for bringing the target company public.

How does a SPAC work?

When a SPAC is formed, it does not identify who the target company is. In its IPO prospectus, the SPAC may share details about the industry or business that it intends to acquire, but there is no obligation to follow through. So if you invest in a SPAC through its IPO, you wouldn’t know the identity of the target company (the one you are ultimately investing in). That is why SPACs are also referred to as blank-cheque companies. In essence, you are relying on the management team that formed the SPAC, commonly referred to as the sponsor(s), to make the acquisition decision.

Think of it as having omakase in a Japanese restaurant – throw out the decision-making, there is only one dish to be served and you will only find out whether you like it or not when it is on your plate. I suppose this probably explains why people would only consider omakase at notable Japanese restaurants. The same goes for SPACs. Investors are more willing to throw caution to the wind and tread in unknown waters if the SPAC sponsors have a track record of success.

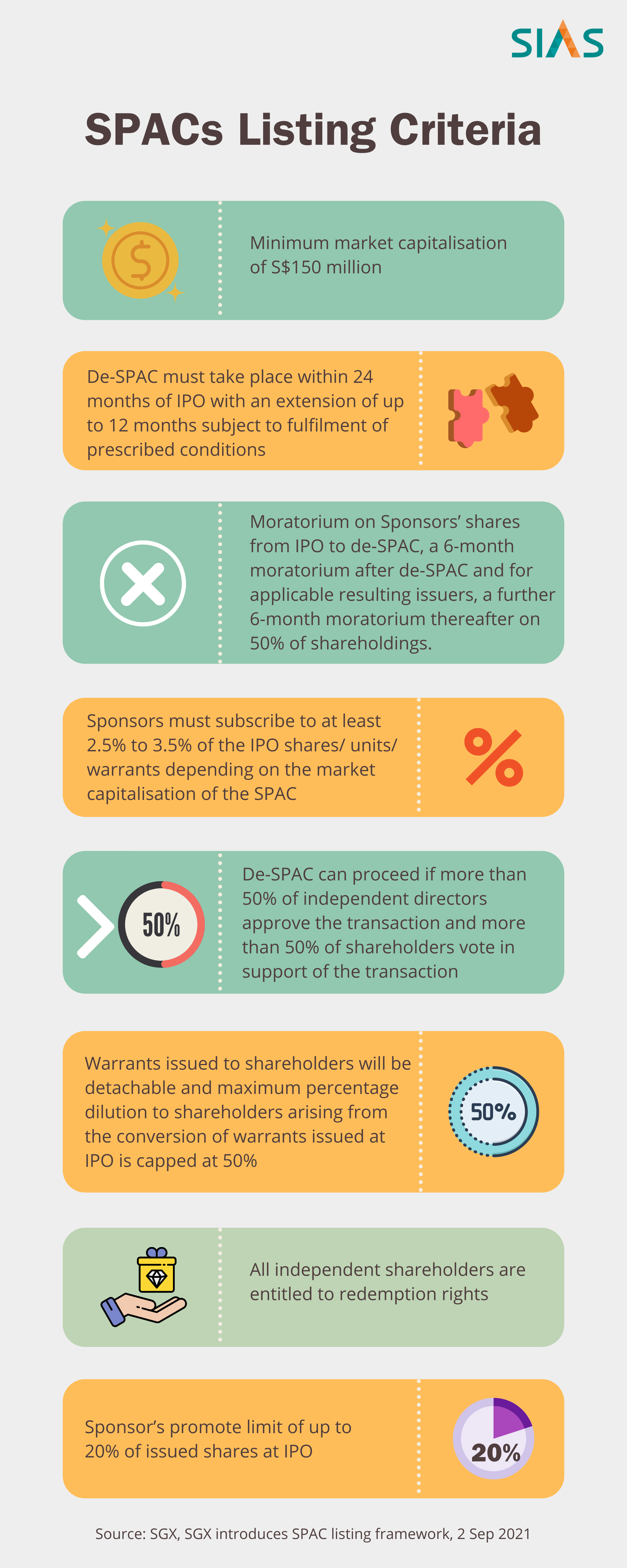

What are the listing criteria for SPAC on SGX?

- Minimum market capitalisation of S$150 million

- De-SPAC must take place within 24 months of IPO with an extension of up to 12 months subject to fulfilment of prescribed conditions

- Moratorium on Sponsors’ shares from IPO to de-SPAC, a 6-month moratorium after de-SPAC and for applicable resulting issuers, a further 6-month moratorium thereafter on 50% of shareholdings.

- Sponsors must subscribe to at least 2.5% to 3.5% of the IPO shares/units/warrants depending on the market capitalisation of the SPAC

- De-SPAC can proceed if more than 50% of independent directors approve the transaction and more than 50% of shareholders vote in support of the transaction

- Warrants issued to shareholders will be detachable and maximum percentage dilution to shareholders arising from the conversion of warrants issued at IPO is capped at 50%

- All independent shareholders are entitled to redemption rights

- Sponsor’s promote limit of up to 20% of issued shares at IPO

Source: SGX, SGX introduces SPAC listing framework, 2 Sep 2021

Why are SPACs gaining popularity?

SPACs offer a shorter route for a company to go public and receive a capital influx faster than it would have with a conventional IPO. Adding to its attractiveness, there is also flexibility for the target company to negotiate its fixed valuation with the SPAC sponsors. The conventional IPO, on the other hand, does not offer room for negotiation – investors will look for other companies if they find the offered terms unsatisfactory. Toss in market volatility attributed to the Covid pandemic and the trepidation of how it might adversely affect the IPO, SPACs probably look like a shiny route, especially to start-ups.

A parting thought for investors who are considering SPACs. If you are not a fan of blind boxes, SPACs is probably not for you.

Article contributed by Dr Jesslyn Lim, Lecturer, Accountancy Programme, Singapore Institute of Technology (SIT)

Subscribe to Newsletter

Subscribe to SIAS Mailing List and get updates to all upcoming events and news

By clicking submit, you agree to our privacy statement, collection, use and/or disclosure of your personal data to the extent necessary to provide you with this service.