Exchanged Traded Funds (ETFs)

Exchange Traded Funds (ETFs) are often described as instruments that give investors the benefits of diversification at a low cost. While this may be attractive, it is important to know that ETFs, being investment products, are not free from risk elements.

It is also important to know that not all ETFs have the same structure and level of complexity. Some ETFs come with more complex structures, and may not invest directly in the assets or components of the indices that the ETFs track. Depending on the structure of the ETF, some ETFs are not able to replicate the returns of the underlying asset or index as closely as others, and some ETFs may be exposed to more risks than others.

This Guide aims to help you understand what ETFs are and what you should consider before investing in them. It highlights the benefits and risks of investing in ETFs, what you should look out for in the prospectus and other important information.

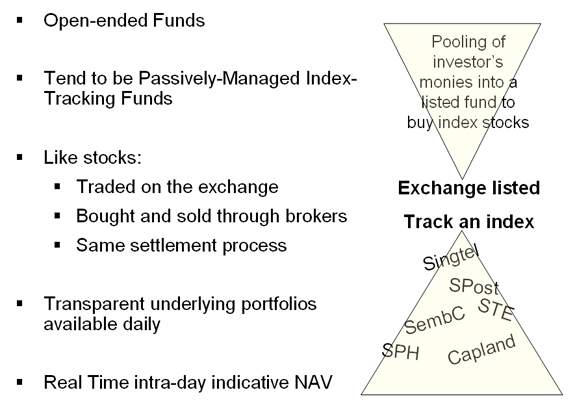

ETFs are open-ended investment funds listed and traded on a stock exchange. Similar to trading any stock, you can buy and sell ETFs through any stock broker at market price throughout the trading day.

The objective of an ETF is to track a specific benchmark such as a stock or commodity index or commodity price. As such, ETFs are passively managed by professional fund managers and their expense ratios are lower than those of actively managed unit trusts since they track and do not try to outperform the underlying benchmark.

Below are examples of assets or indices tracked by ETFs available on the Singapore Exchange (SGX):

• Commodity and commodity index – These ETFs are intended to provide exposure to only one type of commodity or a basket of closely related commodities. As such, they may not be as diversified as ETFs linked to a broad-based equity index.

• Bond index – ETFs can also track a specific bond index. These ETFs provide exposure to the fixed income market.

• Equities

– Long stock index – Some ETFs track the movements of a stock index, such as the Straits Times Index (STI). This means that if the index increases in value by 2%, the ETF is intended to increase by 2%, less any fees.

– Inverse (or ‘short’) index – These ETFs track the movements of a short index. The short index moves inversely to its corresponding long index on a daily basis. So if the long stock index drops by 2%, the short index will increase by 2% less any fees. However, this relationship holds only on a day-to-day basis. The movement of a short ETF may not be equal to the simple inverse of the long index when measured over a period of more than one day. These ETFs are generally not intended for long term investments and are generally not suitable for retail investors who plan to hold them for longer than one day, particularly not in volatile markets.

ETFs are continually being listed on SGX, covering worldwide equity markets such as Singapore, India, North Asia, ASEAN, United States, Eastern Europe, Latin America and emerging markets, as well as commodities including gold.

Get the latest list of ETFs listed on SGX on ww.sgx.com

TIP: Do not assume that all ETFs come with low risks and are intended for long term investing. Read your prospectus and research reports to understand three key areas:-

– The investment objectives (in particular whether the specific ETF you intend to invest in is meant to track indices on a daily basis only and thus only suitable for short term investing);

– The underlying exposure; and

– Its expected returns and volatility.

ETFs can be structured differently to track the same underlying index. For example, some ETFs replicate the index by investing in the index’s component stocks. Others may invest in a representative sample of stocks from the index they are designed to track.

Some ETFs may use other more sophisticated instruments like swaps and participatory notes in addition to holding a basket of representative stocks or collateral. This may be because they wish to track the underlying index more efficiently or because it is not possible for the ETF to invest directly in the index’s component stocks.

However, this exposes the ETF to counterparty risk from the swap counterparty or participatory note issuer. This means that in the event of bankruptcy or insolvency of the counterparty, the ETF may incur losses and the extent of loss will depend on fund’s exposure to the swap counterparty. For example, UCITS III compliant ETFs(1) are allowed to use derivatives (including swaps), although they must limit their exposure to a single counterparty to 10% of its net asset value (NAV), most commonly via the posting of collateral. In other words, the fund is limited to the losses that are related to the default of the swap counterparty, to a maximum of 10%, should the collateral maintain its value after a default. There are also other ETF structures which require posting of collateral by the swap counterparty to mitigate the extent of loss, should the counterparty default.

(1) UCITS III is the regulatory regime for funds in Europe. UCITS refers to undertakings for collective investment in transferable securities.

TIP: Always find out how the ETF you are considering works. Remember that not all ETFs have the same structure and level of complexity.

- Read the “Investment Approach” and “Risks” portions of your prospectus for information on the various risks of the specific ETF you intend to invest in. Note that the risk elements may differ greatly between ETFs depending on their structure.

- Consider if the ETFs structure and risk profile suit your risk appetite and investment time horizon.

- Do not invest in an ETF if you do not understand or are not comfortable with the structure.

dvantages of ETF!

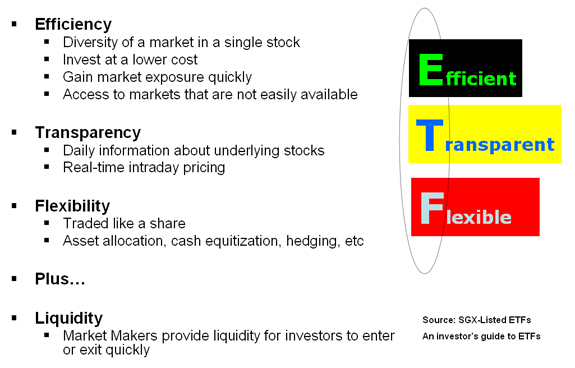

Benefits of ETFs

Diversification: Compared to stocks, ETFs on stock indices allow investors to avoid stock-picking by providing exposure to a diversified portfolio of stocks through a single transaction at an affordable price. However, not all ETFs are broadly diversified. The extent of diversification benefits depends on the constituents that make up the fund portfolio. For example, ETFs that are meant to track the performance of a single commodity or a basket of closely related commodities will not be as diversified as those broad-based equity index ETFs.

In the case of long only country indices ETFs, they retain relevant exposure to the country or market. For example, a country’s key index like the Straits Times Index (STI) for Singapore aims to reflect the economic composition and market structure of the economy. Over time, index providers adjust the indices to maintain this relevance according to the rules set in the index methodology. As such, investors holding these ETF units will be appropriately diversified.

Adding ETFs in your investment portfolio can help diversify unsystematic risk. This refers to the risk of price change due to the unique circumstances of a specific stock as opposed to circumstances in the overall market. However, as with all other investment products, ETFs cannot eliminate market risk. Refer to the section on Risks of ETFs for more information

Cost Efficiency: Compared to unit trusts, investing in ETFs is more cost-efficient as investors do not need to incur the typical sales charge of 3% to 5%. The brokerage commission paid is similar to that paid when buying or selling stocks. The expense ratios for ETFs also tend to be lower than unit trusts, usually due to the annual management fee being typically less than 1%. Management fees for unit trusts generally range between 1% and 2%.

Transparency and Flexibility: The process of buying or selling an ETF is transparent and flexible, just like trading stocks listed on the exchange. Investors can access information on the ETF prices and trade ETFs throughout the trading day. Moreover, investors can employ the traditional techniques of stock trading including stop-loss orders, limit orders, margin purchases, etc. This transparency and flexibility cannot be achieved with unit trusts as investors can only transact at one price calculated at the end of each day.

See Table 1 for a comparison of features between ETFs, stocks and unit trusts.

Table 1: Comparison of features between ETFs, Stocks & Unit Trusts

|

ETFs |

Stocks |

Unit Trusts |

|

| Diversification |

Yes |

No |

Yes |

| Sales Charges |

None |

None |

3 – 5% |

| Management Fees |

Less Than 1%* |

None |

1 – 2% * |

| Intra-day Price Transparency |

Yes |

Yes |

No |

| Traded Through Broker |

Yes |

Yes |

No |

| Brokerage Commission |

Yes |

Yes |

None |

| Settlement |

Third Business Day after Trade Date |

Third Business Date After Trade Date |

Upfront |

*ETFs and other unit trusts may have to incur other expenses, such as legal or trustee fees, which may be payable from the fund separately from the management fees.

Some of the risks associated with investing in ETFs include:

Investing for longer than the Intended Tracking Period: Inverse or short ETFs are intended to track the movements of a short index. The short index moves inversely to its corresponding long index on a daily basis. This means that the performance of the short index may differ greatly from the inverse performance of the long index when measured over a period of more than one day. These ETFs are generally not intended for long term investments and are generally not suitable for retail investors who plan to hold them for longer than one day, particularly not in volatile markets. Investors should familiarise themselves with the investment objective in the prospectus to see if the specific ETF they intend to invest in is meant to track indices only on a daily basis.

Market Risk: Investors are exposed to market risk or volatility of the specific benchmark which the ETF tracks. For example, the performance of an ETF tracking the STI will be directly affected by the price fluctuations of the constituent stocks of the STI.

Counterparty Risk: Where an ETF uses a swap or participatory note structure, investors are exposed to counterparty risk. This means that in the event of a bankruptcy or insolvency of the counterparty, the ETF could incur significant losses. For some ETFs registered as UCITS III, this loss could be limited to 10% of their total NAV, but for others, this loss could be much larger.

Tracking Error: The fund manager of the ETF may not be able to exactly replicate the performance of the specific benchmark due to various fees, investment constraints, timing differences and other factors. This is known as tracking error. As a result, the change in the NAV of the ETF may not exactly follow the price changes of the benchmark.

Market Price not reflecting NAV: The NAV of the ETF may itself be different from the market price, which is affected by demand and supply. The designated market maker works with the fund manager to create new units or redeem units to meet market demand and bring the market price in line with the NAV of the ETF. However, this may not erase the difference between the market price and the NAV entirely.

Foreign Exchange Risk: For ETFs denominated in foreign currencies, investors should be aware that foreign exchange rate fluctuations may affect the returns if they wish to receive their returns in Singapore Dollars. In addition, some of the assets of the ETFs may not be denominated in the same currency the ETF is traded in.

Liquidity Risk: As with all investments, investors should be aware of liquidity risk – the risk arising from difficulty in buying or selling units in an ETF. Liquidity in ETFs is usually provided by a market maker who will provide continuous bid-ask prices throughout the trading day. However, in the event that the market maker fails to perform its duty due to insolvency or other considerations, liquidity in the ETF is not guaranteed. The ETF may then have a large spread between bid-ask prices. However, unit trusts generally have better liquidity as the fund manager is legally bound to redeem units on each dealing day, except in extreme circumstances described in the prospectus.

Conclusion

As with any other investment product, investors should also take time to understand the product and consider whether it is suitable for them. Here are a few key things you should check before deciding whether to invest in an ETF.

1) What does the ETF track?

Do not assume that all ETFs come with low risks and are intended for long term investing. Read your prospectus and research reports to understand three key areas:

- the investment objectives (in particular whether the specific ETF you intend to invest in is meant to track indices on a daily basis only and thus suitable for short term investing);

- the underlying exposure; and

- its expected returns and volatility.

2) How is the ETF structured and what does it invest in?

Remember that not all ETFs have the same structure and level of complexity. Read the “Investment Approach” and “Risks” portions of your prospectus for information on the various risks of the specific ETF you intend to invest in. Note that the risk elements may differ greatly between ETFs depending on their structure.

Do also find out:

- Who is the Fund Manager and the Market Maker? (For e.g. manager’s track record in managing ETFs, the quality of market making by the market maker in terms of providing competitive bid/ask spread. If either fails to perform their duty due to insolvency or other considerations, liquidity in the ETF is not guaranteed.)

- What are the trading specifications (i.e. board lot size & currency denomination)?

- What are the expected costs (i.e. brokerage commission, management fees & expense ratio)?

3) What level of tracking error is likely to occur and how would this error impact your returns?

Ask your financial adviser or broker:

- how you can monitor the tracking error regularly;

- what measures are in place to manage such errors; and

- what risks and costs come with these measures.

4) Does the ETF’s structure and risk profile suit your risk appetite and investment time horizon?

5) How does the ETF you are considering compare with other investment options?

Last but not least, if you find that you do not understand the ETF or are not comfortable with its structure and risks, do not invest in it.

This information is provided by the Singapore Management University Sim Kee Boon Institute for Financial Economics and the Monetary Authority of Singapore (MAS) as part of the MoneySENSE national financial education programme.